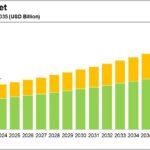

India is embarking on an ambitious plan to invest $87 billion in the petrochemical sector over the next decade, as part of its strategy to boost self-reliance and meet growing domestic and global demand for high-value chemical products. The initiative, announced by the Ministry of Chemicals and Fertilizers, aims to significantly expand the country’s petrochemical production capacity, with a focus on key industries such as plastics, polymers, and specialty chemicals.

The investment will drive the establishment of state-of-the-art petrochemical hubs, with key projects led by major public sector undertakings like Bharat Petroleum Corporation Limited (BPCL) and Indian Oil Corporation Limited (IOCL). These projects include the development of advanced refineries, integration of petrochemical complexes, and the production of sustainable and biodegradable materials to align with global sustainability goals.

This massive infusion of capital also seeks to reduce India’s dependence on imports, bolster exports, and create millions of jobs across the value chain. However, the initiative faces challenges such as fluctuating energy prices, raw material supply constraints, and increasing environmental regulations. To address these, the government is promoting public-private partnerships and encouraging the adoption of green technologies.

With this investment, India aims to position itself as a global hub for petrochemicals, driving economic growth and enhancing its role in the international chemical value chain.

{kind=link}